Table of Contents

INVESTING MISTAKE 1. LEVERAGE

Improper use of leverage is one of the most recurring investing mistakes.

Trading with leverage means buying more than you could with your cash available. For example, if a company’s stock is traded at $100 and you own $1000, 10 is the maximum number of shares you can buy. A 5x leverage would allow you to buy 50 of those same shares (totaling $5000 of which $1,000 of equity and $4,000 of debt), a 100x leverage would equal 1000 shares etc.

But who anticipates that capital in leveraged operations? Generally, the investment platform which in turns borrows from a bank or use its own capital.

Leverage makes you lose money in at least three ways:

1. Leveraged investments have costs in terms of interest expense: as outlined earlier, in levered trades, the amount you do not own is lent to you, which means that passive interest costs accumulate on a daily basis, they can be quite expensive and erode investment profits.

2. Leverage amplifies spread costs: the main source of revenue for market makers – istitutions allowing buyers and sellers to exchange securities – is the spread between the price paid to buy a security (ASK price) and the price received for the sale of the same security (BID price). The spread typically fluctuates between a few basis points to several hundred points, depending on the liquidity of the instrument and the efficiency of the market maker.

Leveraging will increase spread costs, as you will actually pay the spread as many time as the leverage employed.

3. There is inherent volatility in financial markets as securities are constantly traded, and prices change frequently. Sometimes asset prices swing substantially, even over a short period of time. Leverage exposes x times more to price movements: a 5% price movement on a 10x leverage position has a 50% impact.

Money, or equity, used for leveraged transactions is called margin; a position is automatically closed if all or only part of the margin is used.

As shown in the example below, this could mean that a leveraged position can be forcibly closed even if that investment would actually be profitable, leading to a twice negative investment result: lost profit opportunity and realized loss.

A portfolio without leverage will help you reach your investment goals pretty quickly. Instead, an unexpected margin call on a levered capital could ruin a well-made portfolio.

INVESTING MISTAKE 2. NOT INVESTING REGULARLY

Most people fail to realize how quickly they can develop a sizeable investment account simply by making modest but regular investments, missing out on the magic of compounding.

Here’s an illustration of compounding at work: assume you open an investment account with an initial €5,000 investment, and the portfolio provides a 12% annual return on investment; you make no further deposits to the account. In 10 years, your pot will have grown to over €15,500, more than tripling your money. Not bad.

But now assume that you make one tiny adjustment, contributing an additional €50 monthly to the account. Figuring in €50 monthly contributions, in 10 years, your investment account will have grown to €27,300 – almost double the account size that you’d have had without making any additional contributions. Suppose you bump those monthly contributions up to €100 per month. In that case, the 10-year account total will balloon to over €39,000 from an initial investment of just €5,000, followed by making modest additional contributions regularly.

Regularly investing even small amounts of money is a habit worth cultivating, a practice that will pay off handsomely.

INVESTING MISTAKE 3. LETTING EMOTIONS TAKE THE LEAD

The number one killer of investment return is emotion.

Since money is at stake, investing has been known to affect emotional well-being. That’s why keeping a level head when investing is essential, as emotions can cloud judgment.

The hypothesis that fear and greed rule the market is absolutely true. However, intelligent investors should not let fear or greed control their decisions. Instead, they should focus on the bigger picture. An investor ruled by emotion may see this type of negative return and panic sell when they probably would have been better off holding the investment for the long term.

Furthermore, patient investors may benefit from the irrational decisions of other investors.

INVESTING MISTAKE 4. INVESTING BLINDLY

Behind one strong investment recommendation, there might be months, if not years, of work. That kind of 24/7 work. So what explains all these free stock recommendations on the web?

Let us explain once and for all so that you will never forget why there is so much fuss around free buy/sell signals.

Reason number 1: SEO.

Search Engine Optimization entails techniques used to attract more traffic to a website to ultimately drive sales and advertising. Writing content is one of the main pillars of SEO.

Most of the time, free articles on the best investments to buy are written and published to increase visibility and attract readers. But unfortunately, these articles seldom enclose valuable insight and sometimes can lead to awful investment decisions.

Reason number 2: MORE INVESTMENT TRANSACTIONS = MORE REVENUE.

Investment brokers, trading platforms, and their affiliates earn money mostly from spreads (see investing mistake 1) and transaction costs; the latter are usually fixed or variable fees payable on every trade. This alone explains why there is a general incentivization to persuade investors to undertake more trades.

Once you begin investing, you’ll likely get unsolicited advice from stock trading sources, blogs, forums, etc. However, you should never unthinkingly invest in free tips or recommendations, even if they sound appealing.

INVESTING MISTAKE 5. TAKING TOO MUCH, TOO LITTLE, OR THE WRONG RISK

Investing involves taking some level of risk in exchange for a potential reward. Taking too much risk can lead to significant variations in investment performance that may be outside your comfort zone. Conversely, taking too little risk can result in returns too low to achieve your financial goals.

Ensure you know your financial and emotional ability to take risks and recognize your investment risks.

INVESTING MISTAKE 6. FALLING IN LOVE WITH A COMPANY

Too often, when we see a company we’ve invested in do well, it’s easy to fall in love with it and forget that we bought the stock as an investment.

Always remember, you bought this stock to make money. If any of the fundamentals that prompted you to buy into the company change, consider selling the stock.

INVESTING MISTAKE 7. LACKING PATIENCE

Expecting a portfolio to do something other than what it is designed to do is a recipe for disaster. This means you must keep your expectations realistic about the portfolio growth and returns timeline.

A slow and steady approach to portfolio growth will yield greater returns in the long run.

INVESTING MISTAKE 8. HIGH TURNOVER

Investment turnover – jumping in and out of positions – is a return killer.

Unless you’re an institutional investor with the benefit of low commission rates, the transaction costs can eat you alive, not to mention the short-term tax rates and the opportunity cost of missing out on the long-term gains of other sensible investments.

Do not overtrade.

INVESTING MISTAKE 9. ATTEMPTING TO TIME THE MARKET

Trying to time the market kills returns. Successfully timing the market is extremely difficult, if not impossible. Even institutional investors often fail to do it successfully.

The investment literature has plenty of studies showing that, on average, the investment policy decision explains about 95% of the variation of returns over time. In layperson’s terms, this means that most of a portfolio’s return can be explained by the asset allocation decisions (the investments and their allocations) you make, not by market timing.

An investor that was out of the market during the top 10 trading days for the S&P 500 Index from 1993 to 2013 would have achieved a 5.4% annualized return instead of 9.2% by staying invested. This difference proves that investors are better off contributing consistently to their investment portfolio rather than trying to trade in and out in an attempt to time the market.

INVESTING MISTAKE 10. REACTING TO THE MEDIA

Plenty of 24-hour news channels make money by showing “tradable” information. It would be foolish to try to keep up. The key is to parse valuable information out of all the noise.

Successful and seasoned intelligent investors gather information from several independent sources and conduct their own proprietary research and analysis. Using the news as a sole source of investment analysis is a common investor mistake because it has already been factored into market pricing by the time the information has become public.

INVESTING MISTAKE 11. GETTING EXCITED BY STOCKS THAT ARE SKYROCKETING

Chasing the trends is a common mistake investors make. Investors follow the next hot stock, not knowing why they are choosing a particular investment other than “someone else says it is awesome.”

Legend investors find their next big investment opportunities starting from the stocks trading at their 52-week low, not when they are at their highest.

Rather than following the herd, it is best to do the opposite.

INVESTING MISTAKE 12. CONSTANTLY WATCHING THE MARKETS

Of all the mistakes we heard, this one came up the most. While it’s normal (and generally advised) to keep an eye on what’s happening in the overall economy, it’s easy to get swept up in the excitement, doom, and gloom of it all.

The markets are constantly moving, and trying to follow along in real time can lead you to continue checking or changing your investments when you’re better off leaving them alone for the long haul.

You’re likely to perform worse than if you just stuck with your original strategy in the first place; viewing negative performance without context can lead to rash decision-making, while positive performance can instil overconfidence.

Investors should avoid tracking their performance (both good and bad) too frequently. While getting instant information on your portfolio’s progress is easier than ever, it doesn’t mean it’s necessary.

If we were running a marathon, tracking our mileage in quarter-mile increments wouldn’t make sense. The same can be said about long-term investing, particularly in retirement accounts which traditionally have the most extended time horizon.

Look at your investments not more frequently than quarterly, which should be more than enough.

INVESTING MISTAKE 13. FOLLOWING GENERAL ADVICE FROM SOCIAL MEDIA

Don’t take investment advice from those who don’t know your personal financial situation. For example, you may feel pressured by someone on social media to start investing in a specific company, but they aren’t clued to what other better investment options you may have.

INVESTING MISTAKE 14. TAKING INVESTING AS GAMBLING

Some trading strategies look very much like gambling.

Many people like the emotion of winning their bet multiple times or eventually losing all their pots; we reckon that gambling may be fun overall.

Remember to limit your speculative bet to a maximum of 10% of the amount of your portfolio. You’ll win and lose some, but most importantly, you might learn valuable lessons and prevent yourself from doing silly things with your earnest money.

INVESTING MISTAKE 15. SEEKING OUT EXOTIC PRODUCTS

Leveraged and inverse leveraged funds, to mention the most common exotic products you may find during your searches, can seem like a great way to triple your money quickly, but they carry a ton of risk. Do you know what “inverse leveraged” mean? Exactly.

Stick with investments that are comprehensible.

Who We Are

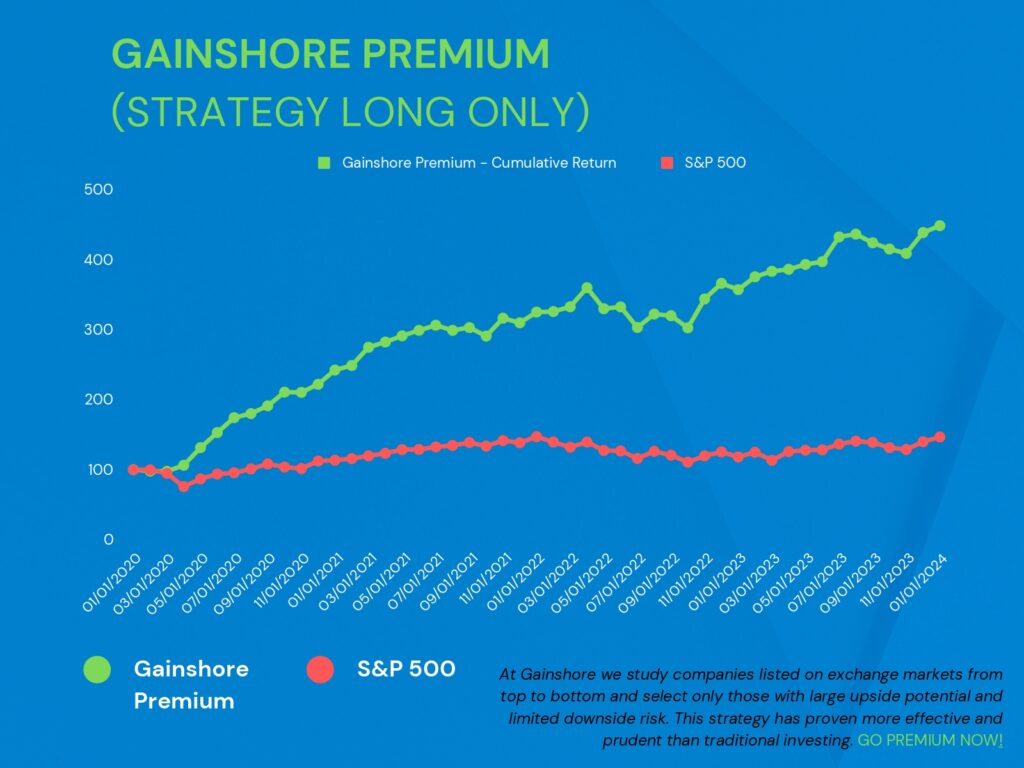

At Gainshore, we aim to help people make the best use of their precious savings by offering our customers the simplest and most cost-effective solution to exploit solid investment opportunities worldwide while protecting them from making unwise decisions that could hinder capital growth or dent their wealth.

Evaluating the underlying business investments we recommend from the perspective of business owners and not mere speculators is our strength.

Our Mission is to be the leading global value-added investment research for beginners and professional investors, positioning ourselves in what we see as the future of the asset management industry: one where the win-win solution stands between do-it-yourself and do-it-for-me.